CareEdge Ratings has released its latest report, “In Q1FY26, Banks’ Profits Buttressed by Treasury Gains.” The analysis reveals that Scheduled Commercial Banks (SCBs) recorded a 3.1% year-on-year (y-o-y) increase in net profit, reaching ₹0.92 lakh crore. This growth was largely supported by treasury gains, including one-off gains from a large private sector bank, which offset muted business growth, margin compression, and weak credit demand. Sequentially, however, profits declined by 2.2% due to margin pressures and increased provisions.

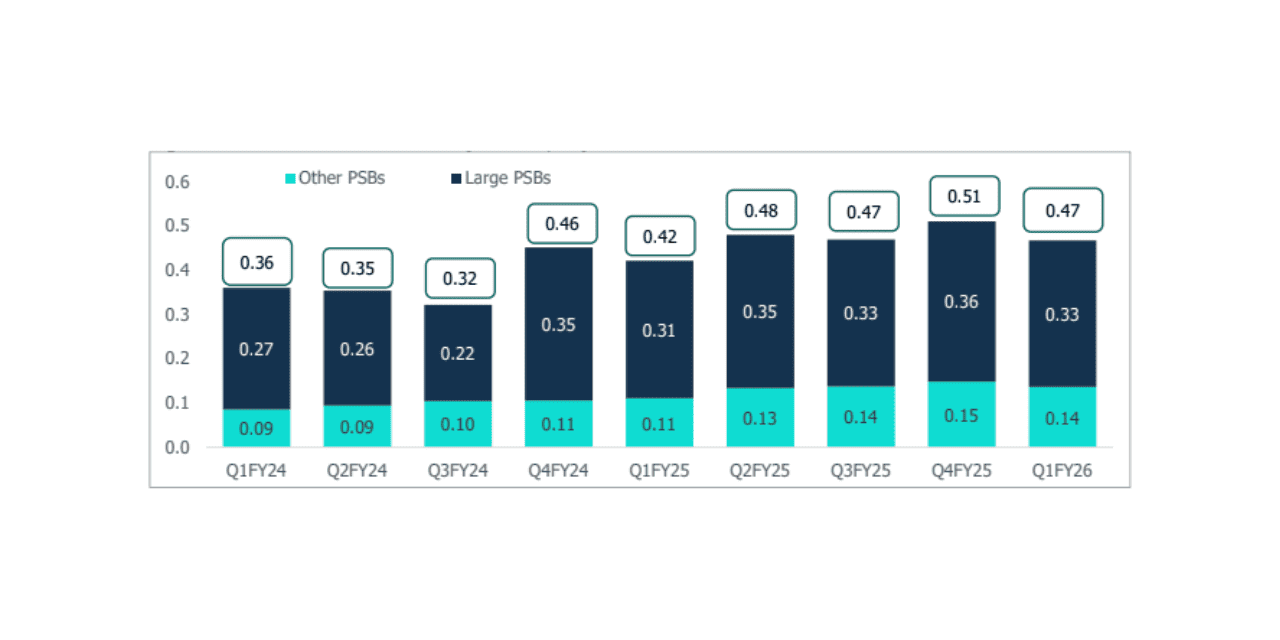

Public Sector Banks (PSBs) saw a robust 10.9% y-o-y growth in net profits, totaling ₹0.47 lakh crore, while Private Sector Banks (PVBs) reported a 3.9% decline to ₹0.45 lakh crore. The dip in PVB profitability was linked to stress in the microfinance and unsecured loan segments, alongside higher provisioning. In contrast, PSBs benefitted from treasury income, strong recoveries from written-off accounts, and growth in the housing segment.

Return on Assets (RoA) for SCBs stood at 1.28% in Q1FY26, down by nine basis points y-o-y, primarily due to margin compression and rising provisions. Capital Adequacy Ratios (CAR) remained strong, with the median CAR of SCBs improving by 145 bps y-o-y to 17.6%, well above the regulatory requirement.

Commenting on the outlook, Sanjay Agarwal, Senior Director, CareEdge Ratings, noted:

“As treasury support fades with stabilising bond yields, banks will need to sharpen focus on earnings and asset quality to sustain profitability. Elevated deposit rates have weighed on funding costs, and while deposit rates have eased recently, NIM compression and rising credit costs may continue to pressure banks. With the festive season approaching, credit demand is expected to drive recovery in the second half of FY26.”

Saurabh Bhalerao, Associate Director, CareEdge Ratings, added:

“PSBs have outpaced PVBs, aided by lower credit-deposit ratios that provided greater lending headroom. However, asset quality challenges in the microfinance and small-ticket loan segments remain pronounced, particularly for PVBs. Capital adequacy continues to remain comfortable across banks, backed by internal accruals and capital raising.”

The report concludes that while treasury gains provided a cushion in Q1FY26, the sustainability of profitability will hinge on credit growth, asset quality management, and cost of funds in the coming quarters.

Banks’ Q1FY26 Profits Rise on Treasury Gains: CareEdge

CareEdge Ratings has released its latest report, “In Q1FY26, Banks’ Profits Buttressed by Treasury Gains.” The analysis reveals that Scheduled Commercial Banks (SCBs) recorded a 3.1% year-on-year (y-o-y) increase in net profit,...

1 min read

Filed under